Publicité

Mixed signals on inflation

Par

Partager cet article

Mixed signals on inflation

Introduction

Inflation is a difficult problem to solve. It has surged since the beginning of the year, much to the dismay of the government which has been unable to fulfil its electoral promise to contain inflation. It has already reached 3.4% by August compared to 3.6% in 2024 and is heading towards 4% by the end of the year. Conscious of its impact on the cost of living especially among low-income households, the government could not remain insensitive to this criticism. Having observed the relentless rise in prices desperately, it came up with a scheme to keep inflation in check. As a last resort, it opted for a direct intervention and implemented the Price Stabilisation Fund, which is more of a palliative than a solution. It does provide some relief in the very short term but does not tackle the real causes of the problem. It is interesting to look at some of the forces at play that will determine our inflation in the months ahead. Some are working in the right direction while a few are less favourable.

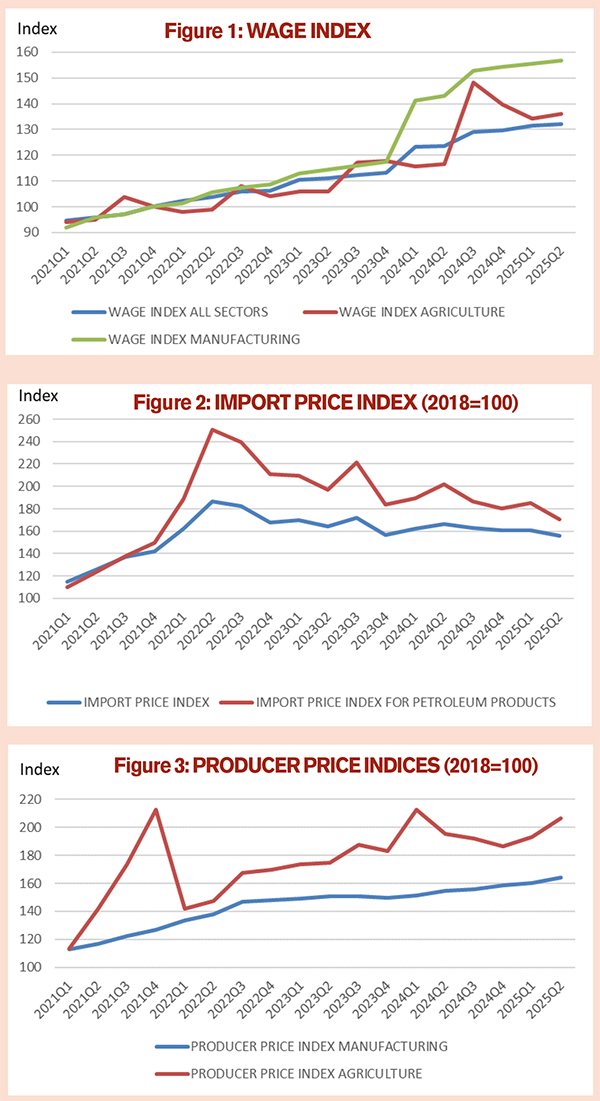

Wage trends

Wages constitute an important component of cost of production and demand. As wages increase, cost of production goes up which is passed on to the consumer in terms of higher prices. The Wage Rate Index has increased by 6.7% between Q4 of 2022 and 2023, and by 14.4% between Q4 of 2023 and 2024. The indices for commodity producing sectors, namely, Agriculture and Manufacturing increased by 40% and 54% respectively in three years (Q4 of 2021 and 2024). Besides generating inflation, the staggering increase in Manufacturing also contributed to the decline in the output and exports of export-oriented enterprises, loss of competitiveness and loss of jobs.

However, there are signs that the wage index increase is tapering off as shown in Figure 1. As a result, we project a lower increase in the wage rate index in the next six months. This is due to the wage policy adopted by the government. For instance, the wage compensation in January 2025 implied a wage increase in line with inflation. Hopefully, the government is doing away with the practice of granting more than one increase in a year, which eliminates uncertainty and unpredictability and helps enterprises better plan their activities, and not become burdened by unforeseen costs accompanied by unveiled threats. In contrast, 2024 was marked by wage compensation of 10% which was 43% higher than inflation in January and a wage adjustment of Rs 2,925 in July 2024, i.e., almost three times more than the annual compensation, and was like a rabbit taken out of a magician’s hat.

Moreover, another factor that has a mitigating effect on inflation is the gradual phasing out of a number of allowances such as Income, Child, School, Pregnancy Care, Maternity, Housing Home Relief Allowances, which reduces demand. Both the wage policy and the reduction in allowances have a dampening effect on consumption. Although consumption expenditure of households and government will increase in nominal terms by 6.6%, in real terms it will grow by 2.9% in 2025 compared to 3.9% last year. Therefore, both cost-push and demand-pull elements are restrained.

Import prices and exchange rates

Import prices are the most important determinant of inflation since more than 60% of imports are directly meant for consumption. Changes in import prices are highly correlated to our inflation. Import prices which reached a high of 186.6 in Q2 of 2022 have been fluctuating within narrow bands ever since. There is a discernible downward trend in 2024 and 2025 as Figure 2 reveals. This trend is also visible for petroleum products which account for almost one fifth of our imports. In recent years, their prices have been influenced mainly by two crises, the war in Ukraine and the Middle East crisis, which explain the sharper fluctuations.

There is a mixed picture when we look at different commodities or commodity groups. Import of crude materials, machinery and equipment in general shows lower price increases than for finished products or consumption items. Prices of some items like live animals, meat and meat preparations and dairy products are on the rise, which translates into higher local prices. Price indices of vegetables and fruits, vegetable fats and oils and cereals are also falling.

It is worth noting the asymmetric behaviour of prices; prices are flexible upward, but rigid downward. Higher import prices are shifted to consumers almost immediately while the opposite may not apply. There may be a time lag for the transmission of lower import prices into lower local prices partly due to availability of stocks. Prices may not even fall and if importers or traders seize the opportunity to raise their own profit margin. The third possibility is that administered prices may stay put with various justifications being provided for the status quo. A notable example is the case of petroleum products with not very convincing arguments.

Allied to import prices is the behaviour of the currency. The rapid depreciation of the rupee automatically fuelled inflation in recent years. The rupee had lost 45% of its value against the dollar between December 2014 and October 2024. This year has been marked by a stability of the exchange rate compared to rapid depreciation of the past. The rupee even appreciated by 1.7% between October 2024 and 3 October 2025. Since 70% of our imports are denominated in dollar, it has a stabilizing effect on inflation. However, the rupee depreciated by over 6% vis-à-vis the euro, which has a relatively lower impact on inflation, given that only 20% of our imports are denominated in this currency.

Producer prices and production

The Producer Price Index is an indicator of inflation at the wholesale level and reflects the rise in the cost of production which sooner or later is shifted to consumers in terms of higher prices. It is a benchmark for consumer prices and gives an idea of the anticipated inflation. The Producer Price Index for Manufacturing is expected to increase by over 6% in 2025 which is twice as high as the increase in 2024 and higher than the expected inflation rate. It will definitely have an impact on the price level. The same trend is noticeable for Producer Price Index for Agriculture in spite of sharp fluctuations due to seasonality of production as Figure 3 indicates.

The Producer Price Index for Agriculture has increased faster than that of Manufacturing; it increased by 9.3% in 2024 but will stabilize at a much lower rate in 2025. Given the trend in agricultural production, it will continue to cushion the impact of other products on CPI. Agricultural production has increased by 29% in the first semester compared to the same period last year. In fact, prices of fresh vegetables rose by over 80% between January and May this year partly due to the effect of drought but has since taken a downward trend. The fall in the prices of fresh vegetables in recent months has toned down the impact of other products on CPI.

Price stabilisation

The government has also implemented the Price Stabilisation Fund with a view to curbing inflation. There was an urgency for such a measure since the government could not remain indifferent to the uptrend in inflation and the hardships faced by consumers. It had to be seen that the government was doing something at the risk of becoming unpopular and drawing the wrath of many stakeholders like consumer associations and trade unions.

In the initial stage, the measure concerns five items which represent about 5% of the CPI weights if we take into account the price of bread, which remains unchanged. There is no doubt that it provides some relief to consumers, but the impact on inflation in general will be marginal. Even if all the funds are utilized, the impact will be at most on 10% of CPI weights. Other products will remain subject to market forces and unbridled. We can only control some prices but not all prices.

Thus, price stabilisation does not solve the inflation problem. It tends to perpetuate the demand for more funds. Inflation is suppressed rather than solved. Administrative measures have never been a cure for inflation. If ever this prop is removed, it will lead to a jump in inflation. It can at best be a temporary expedient only. But the Fund has had a positive psychological effect. It has dissipated the discontent among consumers to a certain extent who welcomed the move.

Indirect taxes

Most of the measures related to indirect taxes in the 2025-26 Budget have already impacted on the CPI, the only remnant of excise duty on sugar sweetened products, namely, chocolate and ice cream takes effect this month but will have minor impact on inflation due to its low weights in CPI. Changes in indirect taxes are normally made at budget time and are not expected to change in the course of the year; as such they will have no further inflationary impact until the next budget.

Conclusion

A glimpse at some of the variables which are the proximate causes of inflation gives an idea of the inflation tendencies in the near future. Some factors are within our control while others are not. It is clear that some factors have a moderating effect on inflation like the exchange rate, declining import prices, higher agricultural output, and the Price Stabilisation Fund, while others are working in the opposite direction, notably, agricultural and manufacturing producer prices, wage increases and indirect taxes. Even if a factor like import price is not within our control, we may minimize its impact by tailoring the right policies, for example, reducing our dependence on imports which can only happen in the medium term. “We have to produce what we consume” should not become a cliché but a reality. In this respect, agriculture has to lead the way not marginally but in a big way. The situation is not as desperate as it seems provided there is consistency in our policies coupled with some bold decisions.

Publicité

Publicité

Les plus récents