Publicité

Growth: mi-figue mi-raisin

Par

Partager cet article

Growth: mi-figue mi-raisin

The National Accounts September update published by Statistics Mauritius indicates that the economic growth for 2025 is projected at 3.1%. Excluding the downturn due to Covid-19 in 2020, it is the second lowest growth in the past 25 years; 2019 recorded a growth of 2.9%. It compares unfavourably with the growth rate of Sub-Saharan Africa (4.1%) or Emerging and Developing Asia (5.2%) and begs the question whether the economy is resilient enough to ensure higher growth. This lukewarm performance should be a cause for alarm as it does not bode well for our future economic prospects especially if we take into account the sharp decline in investment.

Diminishing resilience

At the macro-level, resilience can be assessed by the ability of an economy to bounce back from a severe downturn due to external shocks. The country has been able to withstand crises like Covid-19 and the financial crisis. It took three years for the economy to recover to its preCovid-19 level and resume its erstwhile growth trajectory again. This is due to the fact that it is quite broad-based, and all sectors grew in tandem and contributed to our economic revival. In normal times, we experience another form of resilience with a shortfall in one sector due to unfavourable internal or external circumstances being cushioned or compensated by the expansion of another. 2025 seems to fall in this category, which explains our moderate performance and exemplifies the erosion of our resilience. Some sectors are expanding while others are lagging behind and pin down our overall growth in view of their weight in the economy which we illustrate below and the graphs which give the value-added at constant 2018 prices in billion rupees.

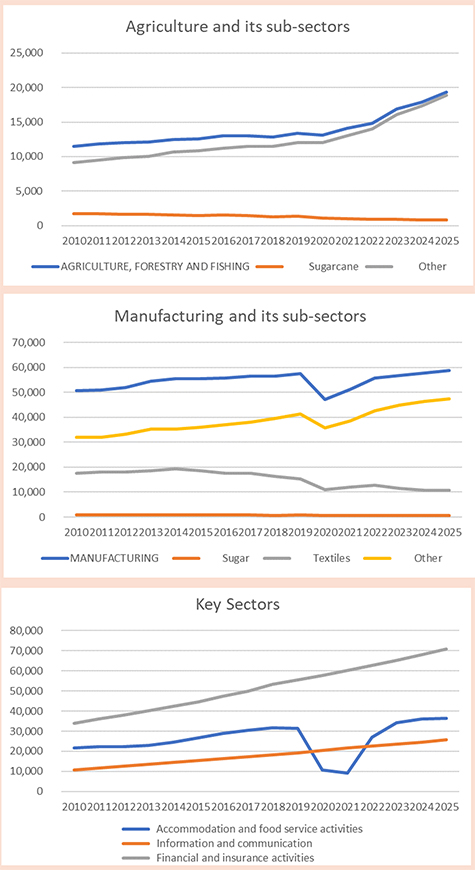

Agriculture is expected to record the highest growth of 8.1% among all sectors or sub-sectors in spite of the long-term decline of sugar cane production, which represents a mere 6% of valueadded in Agriculture, Forestry and Fishing. Sugar cane output has fallen by 50% while Other Agriculture share has doubled between 2010 and 2025. An interesting observation is that the contribution of Other Agriculture, which includes quite a diverse group of products like food crops, livestock and fishing, has compensated fully for the shortfall in sugar cane production in recent years.

This year in particular has been favourable with a high output of food crops in the first half in spite of drought. This diversification drive is a boon for the economy. As I mentioned in an article published in l’express on September 24, 2025, we have to redouble our efforts to optimize agricultural production with multifarious benefits for the country in terms of food security, lower inflation, diminishing imports and improvement of our balance of trade and payments. As SaintExupéry said in Terre des Hommes, “La terre nous en apprend plus long sur nous que tous les livres.” The secular decline of the sugar sector has been more than compensated by production in Other Agriculture, which includes quite a diverse group of products. It accounts for over 90% of value-added in Agriculture. There is scope for Agriculture to become more diversified and resilient if we are able to make some headway in developing the Blue Economy.

Manufacturing which has the highest share in GDP has a very low growth rate of 1.6% due to the combination of two factors, the downward trend in textile and sugar production. Manufacturing is growing at only half of our overall economic growth. Textile production dropped by 43% between 2014 and 2025, a decline which accelerated after 2019. Production for exports, which was our major strength for decades and propelled our economic growth, has now become the weakest link in Manufacturing and pulls down its growth. The Vison Document presented by sir Anerood Jugnauth in 2015 projected a share of 25% for Manufacturing by 2030; instead, it has dropped from 15.4% in 2014 to 12.8% in 2025.

But the long-term decline in textiles is not being compensated by new industries with higher value-added and more technology intensive. The heyday of export led growth is over. In that sense, at the micro-level, our sub-sectors or industries do not have an inbuilt resilience. In fact, there has not been a single new export-oriented enterprise since 2016 as Table 1 shows. The figures speak for themselves highlighting the low priority attached to industrial development by the previous government. Our attempts, if any, to attract new investment has miserably failed calling into question the effectiveness of our institutions to attract productive foreign investment in industry and economic diplomacy. It is still early to pronounce on their effectiveness under the new administration.

Tourism is a major foreign exchange earner, which helps to maintain a positive balance of services in the balance of payments and cushion the yawning balance of trade deficit. It was hit hardest by the Covid-19 pandemic with a sharp dip in output in 2020 and 2021 as the graph on key sectors indicates. It took three years for it to recover fully from the impact of Covid-19 with the number of tourist arrivals attaining its 2019 level in 2024. Tourism which is the third largest sector is struggling to achieve a growth of 2.8%, i.e., half the rate of 2024. The number of tourist arrivals is expected to increase by 3% compared to 4.5% between 2010 and 2019.

Given the direct relationship between sectoral growth and tourist arrivals, there is a lot of homework to be done to attract more tourists. The choice is clear. We can either be content and complacent with our moderate or low growth or adopt a more aggressive and ambitious policy to explore avenues for higher growth. In this industry as well, we see an undue concentration in traditional markets for decades, which might have reached a saturation point with limited scope for boosting growth. Alternatively, growth can be enhanced if we can diversify our markets and build greater resilience. In this respect, we have to learn from the experience of some of our competitors. Although the emergence of Tourism was a private sector initiative the government has played a leading role in its promotion and expansion. Now that the sector seems to have reached a plateau, government has a bigger role to play, and the markets are more difficult, demanding and competitive.

It is worth adding that almost all sectors and sub-sectors are growing except for Construction, Sugar and Textiles. Our key pillars, namely, ICT, Global Business, Financial Services and Agriculture, are growing faster than the average, but their contribution to growth is pinned down by less performing sectors like Manufacturing and Tourism as the graphs indicate. It is interesting to note that growth in most sectors is flattening; only the financial sector and ICT display a steady upward growth while Manufacturing, Tourism and many other sectors have only resumed their pre-Covid-19 growth path. There should be a shift to a higher growth path in line with the priority the budget attached to both investment and growth.

Slackening investment

The government aspires to achieve a real GDP growth path of 4-5% by the end of its mandate. A higher level of investment is a pre-requisite for this to materialise. An enhancement of investment leads to higher growth, which in turn spurs more investment. Contrary-wise, a decline in investment today seriously compromises our future growth and renders investment less attractive. While our growth is low, but still positive, investment is already flagging which is more worrying for many reasons. We highlight just a few here.

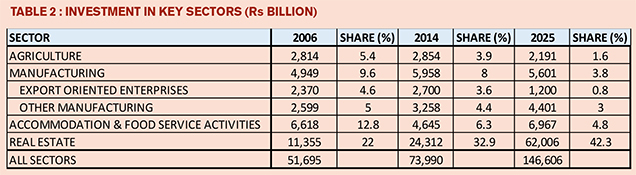

There is a sharp drop in real investment to the tune of 3.4% in 2025. The decline is not limited to one or two sectors, but it is blinking the red signal across most sectors. Among 19 industrial groups, 13 will record negative investment growth, which includes virtually all our pillars. The Investment/ GDP ratio has declined from 20.9% to 19.8% between 2024 and 2025.

Investment in Manufacturing was the third most important sector in 2006, and its share has systematically declined from 9.6% to an abysmally low of 3.8% this year. If we exclude 2020 due to Covid-19, real investment in Manufacturing in 2025 will be the lowest in the past twenty years. The share of investment in export-oriented enterprises has dwindled to less than one percent during the same period.

Investment in Real Estate has increased more than five-fold and its share has almost doubled since 2006 representing 42.3%. It is ten times more than investment in Manufacturing or twenty-eight times more than investment in Agriculture. The bulk of investment is channelled to less productive activities which does not enhance the capacity of the country to produce and export more tangible goods. We thus have an unbalanced composition of investment with productive sectors lagging far behind.

Conclusion

The foregoing shows that a return to the earlier growth trajectory or development path is not enough. It will generate neither investment nor growth. We need more robust and sustainable growth, which at the moment is illusive. Moreover, the investment trends are not very reassuring. The urgency of implementing the New Economic Model cannot be overstated so that we do not have another year of morose growth. In this way, we can strengthen resilience at the micro-level, which in turn will boost investment and achieve higher growth.

The budget is rich in ideas, and their implementation should be expedited. This will be in line with what the budget stated: “We must imperatively unlock growth, contain external deficits, boost productivity and investment to create well-paid jobs for our youth and raise the standard of living for all. We will not let financial restraints stand in the way of economic growth.”

Publicité

Publicité

Les plus récents