Publicité

A brief history of… Brokenomics

Par

Partager cet article

A brief history of… Brokenomics

Mauritius is facing a growing state of economic precarity and vulnerability. In substance, any disturbance or shock — regardless of its magnitude, be it exogenous or internal—has the potential to trigger severe economic repercussions and cause irreversible damage to the country’s social fabric. The urgent need to rebuild fiscal space and engage into bold transformational reforms is critical for Mauritius to regain investor confidence, strengthen public finances, and create a robust foundation for long-term, productive growth.

The not so hidden tip of the iceberg

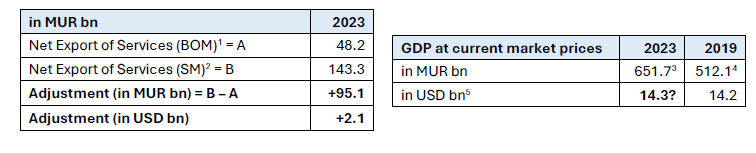

1. As some have argued before, GDP at current market prices has likely been overstated in the recent years. Statistics Mauritius (‘SM’) revised its GDP computation approach in 2023 to reallocate net primary income of some GBC activities and Financial Intermediation Services Indirectly Measured (‘FISIM’) from the Balance of Payments (‘BOP’) produced by the Bank of Mauritius (‘BOM’) to Export of Services, a key component of the country’s output. While the FISIM adjustment (which for all intents and purposes would only represent a fraction of the adjustment) seems, at first hand, understandable and justifiable, the materiality of the overall adjustment of c.15% of GDP remains questionable if only by virtue of the intrinsic nature of GBCs which primarily conduct business outside of Mauritius and whose economic value is generally not attributable to GVA in Mauritius.

-

Notwithstanding its own evident importance, GDP is a pivotal macroeconomic indicator as most other indicators are measured relatively to it. So is Budget Balance or Public Sector Debt (‘PSD’) which officially stood at 78%6 of GDP in 2023. Let alone casting doubt on whether the Mauritian economy has effectively and already recovered to pre-pandemic levels (or not), offsetting this puzzling adjustment would automatically increase PSD to more than 91% of GDP in 2023. This is all the more worrisome considering that the aforesaid PSD ratios do not include (a) “off-balance sheet” USD denominated long term liabilities of some SPV-structured projects estimated at a minimum of 3% of GDP in 2023, (b) the Central Bank’s transfer of MUR73bn to the Treasury7 since 2019, and (c) other money funding of heavily loss-making public sector bodies through central government equity injection.

-

It is pertinent to highlight a few additional important aspects concerning the medium-term outlook of the country's public finances: (a) Special and Other Extra Budgetary Funds, which stood at MUR35.4bn as of June 2021, have experienced substantial net declines since July 2022. By June 2024, these Funds had diminished to MUR13.3bn, with forecasts indicating near depletion by June 2025, (b) the debt servicing of long-term external liabilities associated with the aforesaid SPV-structured projects, negotiated prior to 2018 when the exchange rate was c. MUR35/36 to the USD, has either just commenced or is set to commence at a time when the USD has already crossed the MUR46 mark. Likewise, the servicing costs of all external public debt have and will considerably rise, (c) following a post pandemic technical rebound, the IMF projects the country’s GDP growth to stabilise at around 3.5% starting from 2025, and (d) any additional downgrade of Mauritius’ current borderline investment-grade sovereign credit rating could have serious and long-term repercussions for the country.

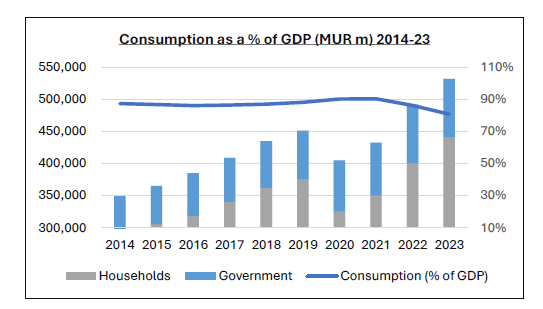

4. In the 10-year period starting from 2014, household and government consumption grew at a CAGR of almost 5% while averaging 87% of GDP. Two major concerns stem from a persistent overreliance on this component of output. Consumption is inherently pro-cyclical and prone to short-term volatility, as it is highly sensitive to changes in consumer confidence, disposable income, and access to credit. Overdependence on consumption increases vulnerability to domestic and global economic fluctuations and reduces the economy’s resilience in times of crisis—any sudden drop has a material impact on GDP, as well as on indirect taxes and fiscal revenues. Furthermore, for a country like Mauritius, consumption is synonymous with economic leakage. This weakens the income cycle and undermines multiplier effects by redirecting spending beyond the boundaries of the domestic economy. As money flows out rather than recirculating within the economy, opportunities for job creation, investment, and income generation are lost, exacerbating trade imbalances, and increasing vulnerability to external shocks.

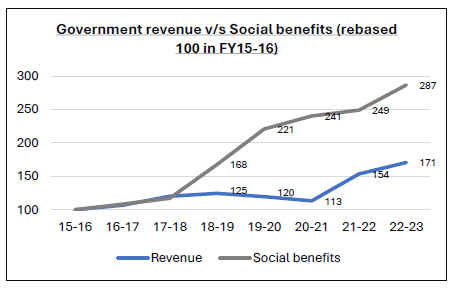

5. Social benefits grew by 187% from MUR19bn to MUR54bn between 2015-16 and 2022-239. In relative terms, those benefits rose from 20% to 32% of total government expenditure during the said period. This staggering increase unequivocally points towards an unsustainable fiscal path. As the dependency ratio continues to increase due to longer life expectancy, the burden of funding these benefits will continue to disproportionately fall on a dwindling base of working-age individuals. Drawing on Austrian school economist Friedrich Hayek’s zealous yet sensible statement, “If socialists understood economics, they wouldn’t be socialists.”, further delaying structural reforms (including the re-engineering of our Welfare State to introduce targeting) to address this growing imbalance will result in Mauritius facing the need for painful adjustments, such as higher taxes, reduced benefits, and even further unsustainable borrowing.

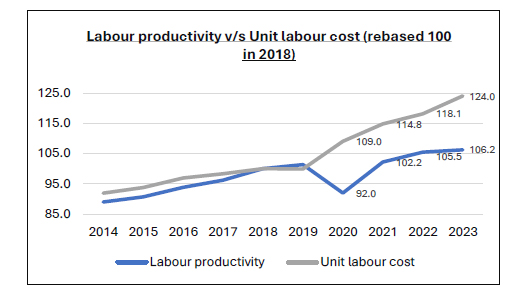

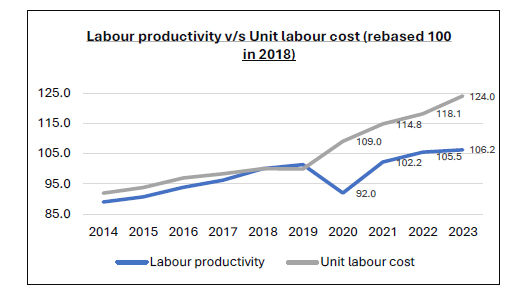

6. Unit labour cost is growing significantly faster than labour productivity since 201910. Between 2018 and 2023, CAGR of unit labour cost (4.4%) outweighed that of labour productivity (1.2%) 3.6-fold. The gap is expected to further widen in 2024 with the increase in minimum wage to MUR16.5k monthly and most importantly with the enactment of Wage Relativity adjustments, effective July 2024, and the expected 14th month bonus payment in December 2024. Rising labour costs without commensurate productivity improvements result in adverse economic consequences, most prominently an erosion in competitiveness, placing additional strain on the economy.

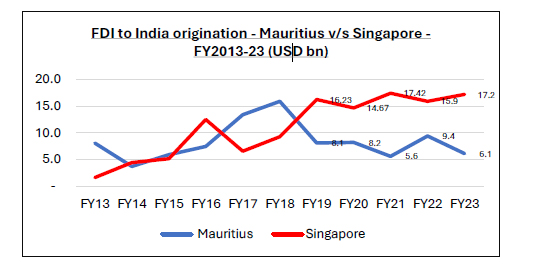

7. USD denominated FDI in Real Estate activities has grown at a CAGR of 10% between 2014 and 2023 while USD denominated FDI excluding Real Estate activities has shrunk at a CAGR of -1.4% during the same period. Save for Real Estate development activities and the acquisition of a few large OMCs by foreign investors between 2016 and 2018, Mauritius has had not much to offer to foreign investors in the past 10 years. An erosion in investor confidence combined with a lack of viable and sophisticated investment opportunities during the said period are plausible explanations behind this trend. The nosedive of the MUR whose downward spiral further accelerated since 2020 and the inclusion of Mauritius in the EU’s list of high-risk third countries have also contributed to the contraction. This is equally illustrated by the significant drop in market capitalisation of listed companies on the SEM since 2020.

8. The trend depicted above in respect of an economy overly reliant on Real Estate activities and consumption is also translated into the Gross Fixed Capital Formation (‘GFCF’) mix. Per National Accounts, 3 economic activities out of a total of 19 i.e. 16% have attracted the lion share of 55%14 of the average investment during the period 2014-23. Those 3 sectors are (a) Real Estate activities, (b) Wholesale and Retail Trade, and (c) Transport and Storage. In stark contrast, while allowance ought to be made that GFCF only captures investment in fixed capital assets, Professional, Scientific, and Technical activities has attracted an infinitesimal 0.5% of average GFCF (2014-23), Education 2.2%, Human Health and Social Work activities 3.6% and Information and Communication 4.1%.

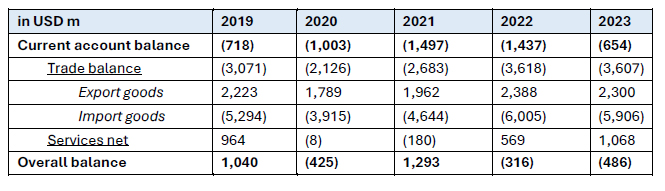

9. The BOP remained, yet again, in deficit in 2023 due to the chronic deficit of its current account15. This structural imbalance is almost certainly the mother of many of our socio-economic ails and one of the primary sources of vulnerability of our country. Between 2019 and 2023, Mauritius has, on average, imported 2.4 times more goods (in value) than it has exported. Net export of manufactured goods and services, once coined as the linchpin of our economic development backbone, remains on average, negative by more than USD2.5bn p.a. during the period. As such, this component is eroding output instead of enabling it.

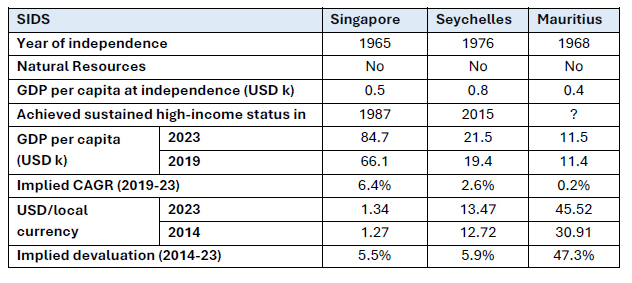

10. Excessive fiscal expansion policies, regardless of productivity and fiscal multiplier imperatives let alone prudential public finances management, had been initiated well before the onset of the COVID-19 pandemic; it being undisputed that the pandemic had the effect of amplifying such expansionary policies and exacerbating the country’s fiscal vulnerabilities. Combined with the uninterrupted deficit of the BOP’s current account, this has led to an unobtrusive foreign exchange control situation, persistent inflationary pressures, and a significant depreciation of the MUR. The following table provides some comparatives between 3 Small Island Developing States.

- The astounding indifference toward the annual publication of the Director of Audit’s report on Government accounts is a striking reflection of the entrenched apathy and blatant disregard for transparency and accountability in the management of public funds. Selected, self-explanatory excerpts from the first 5 pages of his 2022-23 report include the following:

“Over the last three financial years, the National Audit Office (NAO) has repeatedly reported the following issues, amongst others, in Ministries and Government Departments: Weaknesses in Expenditure Control, Deficiencies in Project Management, Lapses in Procurement Management, Deficiencies in Asset Management, Non-compliance with Applicable Laws.”

“The issues highlighted in previous years have again been observed in the financial year 2022-23.” “An analysis of the findings has revealed that the root causes for recurrence of these issues are inadequate accountability mechanism and monitoring system at different levels in Ministries and Government Departments.”

“83 per cent of Ministries and Government Departments have not complied with Section 4B of the Finance and Audit Act in respect of the submission of their Report on Performance within statutory deadline, while 57 per cent of the Key Performance Indicator (KPI) targets set were not met.”

“Audit Committee was not achieving its objectives and Risk Management Framework was not developed”

In sharp contrast, (a) last week in France, former FM Le Maire (who is no longer a MP) and former PM Attal were summoned for a second time by the Commission des Finances du Sénat to provide detailed explanations on the dérapage des comptes publics, particularly regarding the French Government’s revised 2024 deficit forecast of 6.1% of GDP, compared to Le Maire’s own initial budgeted figure of 4.4%, and (b) two weeks ago, the Office for Budget Responsibility, the UK's fiscal watchdog, swiftly released a statement within hours of Chancellor Reeves' October 30th budget address, outlining their significant concerns regarding the long-term impact of the Chancellor’s fiscal expansionary strategy on economic stability and growth.

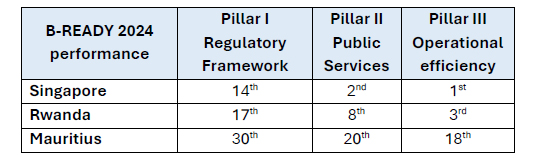

12. Mauritius is mired in the middle-income trap; its economy lacks emphasis on productivity and remains largely undiversified. The two most recent economic pillars, the Global Business sector (introduced in the early 1990s) and the ICT/BPO industry (introduced in the early 2000s), have not been followed by significant new developments. Furthermore, the latest structural reforms of our economy - encompassing fiscal policy, the tax system, business facilitation and ease of doing business - are now over 15 years old. It is pertinent to note that the World Bank, in its B-READY 2024 report, now rates Rwanda significantly higher than Mauritius on all 3 key pillars of business readiness and friendliness. Rwanda ranks 3rd in 50 surveyed countries (including the likes of Singapore, Hong Kong SAR, and New Zealand) for operational efficiency and 8th for public service delivery. Rwanda’s strong performance in the B-READY report stems from its long-term reform agenda initiated in 2008 that has prioritized administrative, legal, and digital transformation reforms aimed at improving the business climate, boosting FDI, and fostering economic growth.

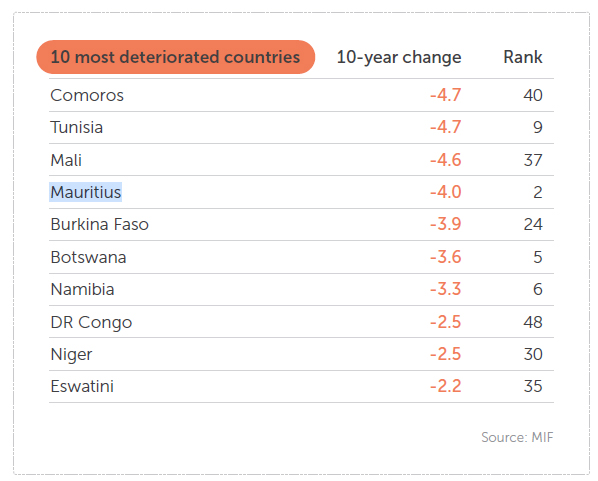

13. In contrast, Mauritius has experienced a notable decline in its standing in the Ibrahim Index of African Governance, a departure from its historic position as the leading African country since the index’s inception in 2007. Since 2020, Mauritius has been overtaken by the Seychelles16, reflecting broader governance challenges. Additionally, Mauritius is now the 4th most significantly deteriorated African country in the past 10 years in terms of Overall Governance performance, with marked deterioration in areas such as Public Administration, Security and Safety, Rights, and Accountability and Transparency.

14. For some time, magniloquent public statements and national budget speeches around Mauritius successively positioning as (i) an education and knowledge hub, (ii) a medical hub, (iii) a seafood hub, (iv) a logistics hub, (v) a blue ocean economy, (vi) an international arbitration centre, (vii) a Fintech hub, (viii) a centre of excellence for Africa, (ix) an investment gateway between Asia and Africa, (x) an Asia-Africa air corridor hub, (xi) a captive insurance services hub, (xii) an international commodities and derivatives exchange hub and as of late (xiii) a virtual assets custodian services hub, (xiv) a biotechnology and pharmaceutical hub and, (xv) a green energy economy have triggered no concrete action and barely yielded any meaningful result. By virtue of its heavy reliance on 2 or 3 key economic pillars, the country is prone to volatility, and vulnerability especially towards exogenous shocks. This underscores the urgent need for economic revitalisation.

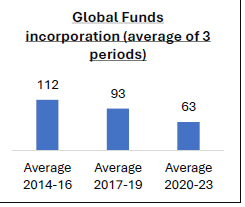

15. The Mauritius International Financial Centre (‘MIFC’) has lost a meaningful share of its attractiveness in the past 10 years in favour of competing IFCs17 due to uncertainty surrounding the jurisdiction, a persistent lack of sophistication in respect of its offerings and an acute mismatch between demand and supply of qualified labour. The drastic erosion of the Mauritius India Double Taxation Avoidance Treaty benefits, the inclusion of Mauritius in the EU list of high-risk third countries and a generally deteriorating macroeconomic environment have heavily weighed on the MIFC. While the Global Business industry continues to grow, albeit at a reduced pace, margins have considerably decreased on account of a major shift towards lower value outsourcing services and a sharp contraction in the incorporation of Global Funds18, known in the sector to be of higher value.

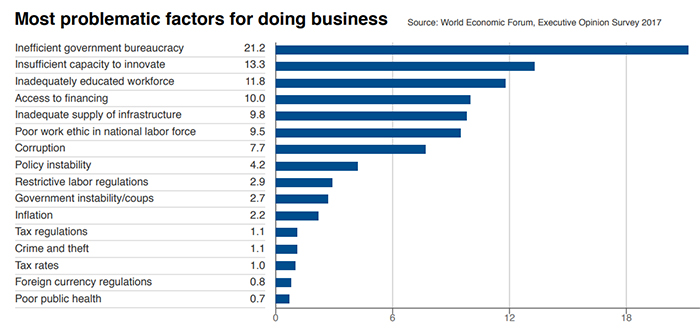

16. In its Global Competitiveness Report 2017, the World Economic Forum already identified “Insufficient capacity to innovate” and “Inadequately educated workforce” as the second and third most problematic factors for doing business in Mauritius. As matters stand today, the Mauritian labour market is, beyond a doubt, characterised by a quasi “perfect” imbalance between demand and supply of labour both in capacity and capability. Skills mismatch, a noticeable trend since the early 2000s, has widened exponentially in the past 6 to 8 years especially in the Financial Services and ICT sectors. The lack of capacity planning and the qualitative decline of our misaligned education system, nivelé par le bas, are the primary reasons that explain this structural deficiency. The Great Immigration of Mauritian high-calibre professionals electing to leave the country for competing IFCs e.g. Luxembourg or mature economies e.g. Canada, which started in 2020, has compounded the problem while contaminating other sectors of the economy. Mauritius is in acute shortage of skilled labour; its talent competitiveness is eroding and its labour costs rapidly escalating. In its 2023 Global Talent Competitiveness Index (‘GTCI’), INSEAD reported a decline in Mauritius’ GTCI ranking from 44 between 2013-18 to 47 between 2019-23, it being noted that the decline is even steeper in 2023 with Mauritius now ranked 51st globally. As to the reasons why Mauritius is so “successful” at exporting its high-value talents, this could not be better explained by the famous French singer J.J. Goldman in his song “Là-bas”, released in 1987 https://www.youtube.com/watch?v=zFwaRmpzvjo.

New balls, please?

The uphill turnaround of the Mauritian economy shall only unfold through the virtuous 5 du travail, de l’éducation, de la confiance, du sens de la responsabilité et de la raison d’être, it being stressed upon that those would only constitute necessary conditions as opposed to sufficient ones. Bold long overdue structural reforms combined with fiscal consolidation are what the economy is in dire need of. And as Milton Friedman once observed “One of the great mistakes is to judge policies and programs by their intentions rather than their results”- the inclination towards correctness should no longer be overshadowed by that of political correctness.

Transformational reforms must go beyond incremental adjustments to tackle the root causes of economic stagnation and vulnerability. The country’s historical reliance on a few key sectors has limited its capacity to adapt to global economic shifts. This narrow economic base exposes Mauritius to external shocks and stifles innovation, productivity, and competitiveness. In Gramsci’s own cynical words: “The crisis consists precisely in the fact that the old is dying and the new cannot be born; in this interregnum a great variety of morbid symptoms 10 appear.” Mauritius now needs to embark on structural reforms that will address long-standing issues of diversification, institutional uplifting and integrity, market inefficiencies, labour market rigidities and global competitiveness.

Fiscal consolidation, akin to the painful reckoning after a soirée bien trop arrosée, represents the unavoidable aftermath of excessive fiscal indulgence. In the words of Warren Buffet: “If you buy things you do not need, soon you will have to sell things you need.”; prolonged spending sprees, accumulating deficits and debt result into fiscal imbalance which, in turn, demands correction. Just as a hangover forces the body to recalibrate after excess, so too does fiscal consolidation compel policymakers to rein in expenditures, raise revenue, and restore fiscal discipline. While the immediate tightening is expected to be uncomfortable, it is the necessary cure to foster long-term economic resilience to ensure future sustainable growth and economic stability.

We can only hope that the new team that has taken charge realises that it now needs to resort to the difficult decisions and act. “Le coeur d’un homme d’Etat doit être dans sa tête” are Napoléon Bonaparte’s wise words which we trust will inspire them…

Publicité

Publicité

Les plus récents