Publicité

Money printing

Our PM misled the House!

Par

Partager cet article

Money printing

Our PM misled the House!

Replying to the parliamentary question (PQ) from MP Ashley Ramdass in respect of allegations of money printing to the tune of Rs 83 billion (bn) by former finance minister Renganaden Padayachy, the Prime Minister (PM) accused the latter of undermining the confidence in our institutions and financial system by his unfounded allegations and misinformation. Renganaden Padayachy upon leaving the Central Criminal Investigation Department on Monday June 1, was claiming that “l’économie, c’est un débat permanent et contradictoire. Ce n’est pas une science figée”.

Agreed that economics’ foundational principles, models and real-world applications are in a constant state of flux. We rely on data and advanced processing capabilities to analyse real-world trends, vastly improving our understanding of the macro-level impacts on society. Ultimately, economics relies heavily on a real-world data to evaluate and improve its theories, although the foundational assumptions driving those theories frequently guide how the data is interpreted in the first place.

What does our data show?

Our data shows that under the previous government (Govt) the Bank of Mauritius (BoM) printed a total of Rs 121 billion, not Rs 181.5bn, as detailed out by the PM in the National Assembly (NA). The total of Rs 121bn is made of:

-

Rs 18bn which was drawn from the Special Reserve Fund (SRF) for repayment of Govt external debt in Financial Year (FY) 2019-20;

-

Rs 55bn transferred to Govt in FY ending June 20 for deficit financing, termed as a one-off contribution to Govt in the BoM’s financial accounts;

-

Rs 48bn as the effective amount of money printed to Mauritius Investment Company (MIC). From the nominal amount of money created, that is, the Rs 81bn credited to the account of MIC at BoM in FY 2020-21, (by simply adding a new item as equity investment on the asset side of BoM’s balance sheet), Rs 33 bn have to be excluded as it is still in the account of the BoM.

This is the total amount of pure money creation. Every other figure advanced is just fake! The amount of Rs 15bn held by BoM in Govt securities is wrongly included by the PM in the quantum of printed money. BoM lending to Development Bank of Mauritius and other institutions, for a total of Rs 12.5bn, is similarly not printed money, as alleged by the PM.

Contrary to what it shamefully

did in Renganaden Padayachy’s case, BoM will not be able to make a complaint to the CCID about the PM’s fake info on money printing, as statements in the NA are legally immune from prosecution. Seriously, the law enforcement authorities in Mauritius have better to do than waste time on technical monetary policy issues. Like Renganaden Padayachy, our PM also does not seem to understand basic monetary economics. But what about the accountability of the BoM officers, the advisers, the Financial Secretary, and team – the very ones who had cooked the GDP and budget figures under Renganaden Padayachy – in clarifying the economic figures and ensuring the integrity of the data that are being disseminated in the NA and to the public?

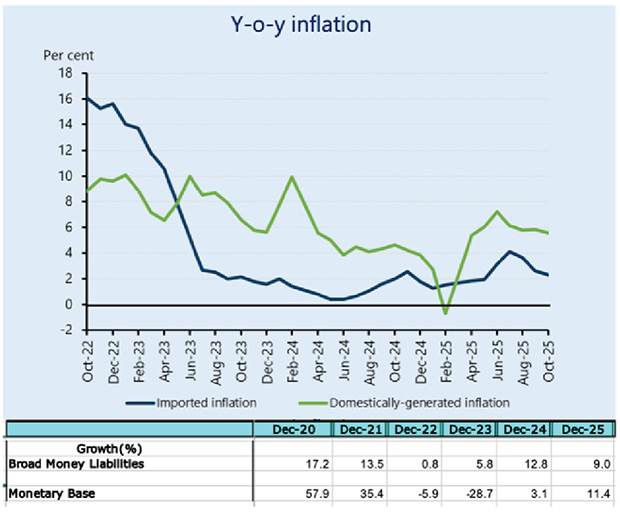

We are also being told that the present difficulties of the BoM are all due to the excessive printing of money by the previous regime! What does our data show? It shows that we cannot keep on blaming the previous regime for the present incapacity of the authorities to mop up the excess liquidity, stabilise the rupee and tackle the inflationary pressures.

The year-on-year (y-o-y) inflation had been coming down under the previous regime itself before picking up again under the new Govt. Both the Broad Money Liabilities and the Monetary Base Growth (MBG) were picking up again in Dec 2025, higher than the nominal growth in GDP and the MBG had reached double digits (see graph below). Moreover, on our weak or non-functioning monetary transmission mechanism, Sameer Sharma reminds us that “lacking absorption, market rates remain stuck at the bottom of the corridor, in negative real territory: the 4.75% policy rate is now merely a figurehead, as the interbank rate, now lower, is the one that truly governs; as for the 125-basis point corridor, it was only used to cope with this ailing balance sheet. The distortion then spreads across the entire yield curve, with the spread between the 10-year and two-year bonds collapsing at the time of issuance – all signs of a non-functioning monetary transmission.”

Stop blaming the other regime for one and all; we have kicked them out once for all; they belong to the past that some are uselessly stuck up with in their repeated paroxysms of scandalous retrospective narratives, insult and indignation that lead us to nowhere; it’s time that they put themselves to the task to restore the Bank’s independence, its technical competence and credibility.

The inference from this startling episode is clear. The mindset at the ministry of Finance and the BoM is still largely driven by cheap and mean political considerations instead of sound economic reasoning. Plus ça change, plus c’est la même chose!

Publicité

Publicité

Les plus récents