Publicité

AMPLIFYING THE POWER OF HELICOPTER MONEY BY THE ORIGINAL MECHANICS OF QUANTITATIVE EASING

Par

Partager cet article

AMPLIFYING THE POWER OF HELICOPTER MONEY BY THE ORIGINAL MECHANICS OF QUANTITATIVE EASING

There is a burgeoning debate currently surrounding the current recession and its prolonged impact on the ailing Mauritian economy. In this article, I shed light on the concept of Quantitative Easing (QE) which has been defined by many economists in a half-baked fashion as an exchange of debt for money.

After an explanation of the original mechanics of QE, I prove its empirical relevance in Mauritius by using data for the period 1980 to 2017. In the final part, I discuss a few options, among helicopter money, that can ensure the growth path of nominal GDP does not suffer from a very severe reversal.

What is Quantitative Easing?

“Quantitative Easing" in its original form, was proposed by Werner (1994) who coined the term when proposing a new form of monetary stimulation for the Bank of Japan during the 1990s recession. As opposed to conventional policy, which relies on increasing money supply or interest rate reductions to encourage lending, in 1994, Werner proposed policies executed at the level of the Bank of Japan that would directly stimulate bank lending to the real sectors. The theoretical proof of his proposition is elegantly explained in his seminal work on the quantity theory of credit (QTC) which he developed in 1992.

MV = PT is known as the traditional equation of exchange for an economy. It measures the total amount that is spent during a period in the real economy is proportional to the total value of transactions. Whilst in monetarist and New-Keynesian perspectives an implicit assumption is often made that all credit flows to the real economy, a significant proportion of bank credit may flow into the purchase and sale of existing financial assets, for example land or property or financial transactions. Therefore, it we exclude those financial transactions, we are left with a direct link between money (M) and nominal GDP (PY) and new version of the equation of exchange namely by MV=PY and in PY there is only GDP transactions.

Moreover, as Werner (1992) and Turner (2014) explain given that banks create the bulk of the money supply by creating credit, the correct measure of “money” (M) should be on the asset side of banks’ balance sheet, more precisely it should be bank credit to the real sector CRb (note that here we exclude bank credit to the financial sector as it entails the buying and selling of existing assets which do not add to GDP). The statement of the Former Governor of the Bank of England, Mervyn King in 2012 is also testament of the money creation capacity of banks, “When banks extend loans to their customers, they create money by crediting their customers’ accounts.” Therefore, if we replace, CRb in MV=PY, we get, CRb V= PY or V= PY/ CRb. This neat result shows that if bank credit to the real sector grows at the same rate as nominal GDP, then this implies that velocity of circulation will be constant. This is the original definition of Quantitative Easing.

Is there a stable relationship between nominal GDP and bank credit to the real economy in Mauritius?

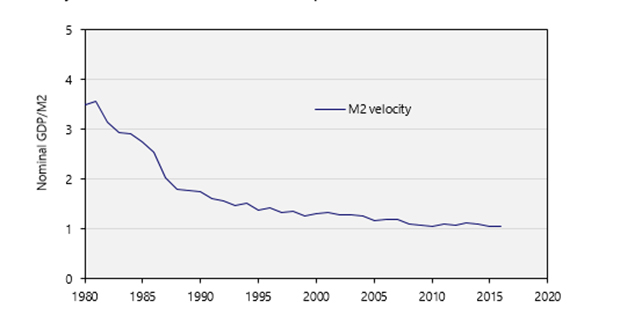

The velocity of money shows the strength of the link between money and the real economy. If there is a strong link between the two, it means that “money” is being used for real sector GDP transactions and hence for productive purposes. This implies that the velocity of money will be constant. However, there is a dilemma which has been observed in many countries around the world i.e., the fall in the velocity of money and Mauritius is not an exception to this rule.

Figure 1. Velocity of broad money (GDP/M2) in Mauritius

The QTC shows that the velocity decline is due to the neglect of non-GDP transactions (financial transactions). Put simply, the velocity of money expresses the relationship between the numerator, GDP and the denominator, money. If the latter rises faster than the former it should be clear that there will be a velocity decline. Therefore, if money created for financial transactions is excluded from the denominator, the QTC predicts that the velocity of money should become stable.

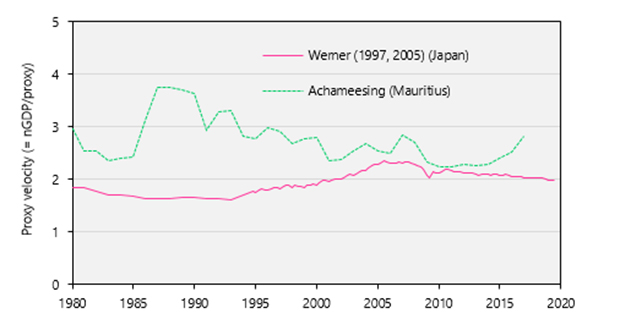

Figure 2. Velocity of proxies of ‘bank lending for GDP transactions’. Source: Werner (1997, 2005), Achameesing (forthcoming).

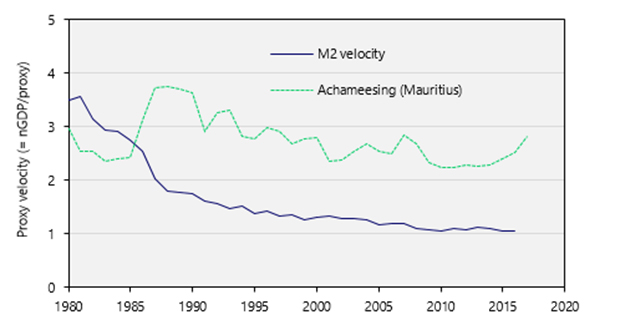

QTC provides a new way of looking at banking in the macroeconomy, by linking bank balance sheets with various measures of expenditures, like GDP. Though monetarist only in origin, it shifts the focus from the liability-side to the asset (or credit)-side of bank balance sheets. Velocity remains roughly stable when its meaning is properly understood, as per the QTC. If financial transactions are assumed to be part of GDP, then there would be an illusion of the velocity decline. This is shown below where bank lending for GDP transactions is in a more stable relationship than the monetary aggregate M2 in Mauritius.

Figure 3. Velocity of ‘bank lending for GDP transactions’ and velocity of money (M2) for Mauritius. Source: Achameesing (forthcoming).

Therefore, by disaggregating bank credit into sub-flows, and identifying those flows that are likely to contribute to GDP transactions, we can explain nominal GDP growth in Mauritius in the 1980-2015 periods quite honorably. Therefore, here I have highlighted the relevance of the QTC as a policy tool, akin to Japan’s post-WWII ‘window guidance’, a powerful instrument in comparison to the orthodox monetary policy instruments of monetary aggregates and the interest rate.

How to stimulate bank credit to GDP transactions?

The next question is how to increase bank credit for GDP transactions. The banking system is composed of the central bank and depository institutions (mainly commercial banks). If the commercial banks are not extending credit to the economy, the central bank can take the baton. The central bank can create money for GDP transactions in several ways:

- Buying government bonds from banks and non-banks. This policy is what the ECB did under its Expanded Asset Purchase Program (EAPP) which started in January 2015. The government issues bonds which are bought by banks and non-banks (insurance companies, pension funds etc.) but are simultaneously repurchased by the central bank. This would be equivalent to central bank granting loans to the government as direct finance to the government is prohibited in many countries. The government then spends the receipts in GDP expenditures and the economy expands according to the QTC. Government can spend on consumption or investment. Both will stimulate GDP but investment is more powerful.

- The central bank guarantees loans by banks to SMEs. This policy is being implemented by the British Business Bank’s, through the Coronavirus Business Interruption Loan Scheme.[1] Since SMEs are the main employer and contribute to GDP transactions, this policy will stimulate GDP.

- Helicopter money. There are two basic ways of doing it:

- Free money for the people. Cash-hand out to the poorest and lowest income groups in the formal and informal sectors which would be credited to their accounts at the commercial banks. This would reduce hardships at the lower level and recipients would most likely spend the money quickly which would contribute to GDP expenditures.

- Helicopter money through the government. This amounts to EAPP but the debt is kept on the books of the central bank and never redeemed, i.e., the debt is effectively written-off. The central bank can do this in moderate amounts, even if its equity becomes negative. Central banks do not have to follow the accounting rules that private entities like commercial banks follow. Helicopter money creates new money for GDP transactions since the government will use the funds to engage in GDP expenditures. The added benefit is that government debt does not increase.

Now the subtlety of modern economics being truly elusive, I would like to point out an important caveat. Generally, there is no guarantee that income received by individuals and businesses would be spent and not saved or hoarded (unless specific conditions are imposed to ensure that they spend and/or invest). Therefore, if government itself spends directly on GDP transactions, it guarantees that the first round effect and subsequent recirculation takes place much faster.

The good news is that money financed deficits would always stimulate nominal GDP without adding to future debt burdens. Monetary finance “is defined as running a fiscal deficit which is not financed by the issue of interest-bearing debt, but by an increase in the monetary base.” In a presentation hosted by the IMF in 2015 entitled “The case for Monetary Finance- An essentially political issue”, leading monetary economist Adair Turner argue that the “technical” case for treating monetary finance as an available policy option is undoubted, and that there are no valid technical reasons for excluding it. Technically, the central bank only registers a decrease in its equity and not an increase in assets as a conventional loan to the government would do. However, Turner severely warns that the political economy of helicopter money could encourage politicians to use this tool in other circumstances to suit their own agenda. Therefore, helicopter money should only be used under exceptional circumstances and very strong restrictions should be imposed upon its use. If helicopter becomes the chosen option, then by using the original mechanics of QE, we can amplify its power. This would be equivalent to a permanent monetization of the fiscal stimulus amount by the central bank which would be strictly spent on GDP transactions. It is important to note that if helicopter money is proposed in isolation without a proper understanding of the real mechanics of QE, then there is a real danger that the money scattered from the helicopter does not fall into the right hands and/or is not spent on GDP transactions or only on consumption (I explain the side effects of this below). Lord Adair Turner who consistently cites the quantity theory of credit is well aware of this fact. If helicopter money is given to businesses to hoard or for non-GDP transactions, then the effects of helicopter money on nominal GDP growth will be mitigated. This scenario is reminiscent of the controversies around the allocation and use of the fiscal stimulus of 2008.

The original work on QE also points to the fact that GDP expenditures have to be nuanced because the effects of consumption and investment on nominal GDP are not equal. For instance, in an extreme case where very large amounts of money are used for consumption, then the side effects of helicopter money in terms of high inflation could become a real problem. However, if a large amount of the helicopter money from the central bank is used for investment, then this will ensure that GDP grows sustainably without high inflation. Therefore, it remains of utmost importance that measures (1) (2) and (3), take into account that profound distinction between consumption and investment to ensure that the appropriate QE combination is implemented. QE makes it clearer that a large part of the money created should (i) encourage the production of new goods and services so that Mauritius grows its way out of this recession and (ii) if government itself spends directly on GDP transactions, it guarantees that the first round effect and subsequent recirculation takes place much faster. Therefore, combining (i) and (ii), public investment on medical facilities and local production of staples to green energy production would be some examples of a potent use of helicopter economy in stimulating nominal GDP growth. Generally, when credit creation is used for productive investments like new technologies, products and services, there is more money in circulation but also more goods and services. In contrast, when there is consumptive credit creation, there is more money but not more goods and services which means that there is inflation without growth. Furthermore, when there is credit creation to purchase existing assets, there is more money in asset markets which causes asset price inflation which economists often refer to as “price bubbles”.

The projections from the Ministry of Finance and Bank of Mauritius predict a contraction of around 7 to 11% of GDP. In a recent newspaper article, Former Governor of the Bank of Mauritius, Mr Basant Roi has vehemently rejected the use of helicopter money as he believes that it might cause high inflation and destabilize the exchange rate. Conversely, the Former Minister of Finance Mr Rama Sithanen has advocated for helicopter money touting that inflation should not be a problem albeit not offering an exact prescription of how much helicopter money should be done. The truth is most likely to be in between of those two diverging opinions. Again, as Adair Turner points out, there is no technical reason why the scale of the impact of monetary finance cannot be managed to produce a desired increase in nominal GDP while having negligible effects on inflation and the exchange rate. With a nominal GDP of Rs 500 billion, it is not advisable that the government exceeds a maximum target of 5% of helicopter money which would be equivalent to Rs 25 billion. If we assume that a maximum of Rs 25 billion of central bank money is spent on GDP transactions with an average estimate of the velocity of circulation of 2.5 (see green line in Figures 2 and 3 above), in the first and second rounds, we would expect a decent impact on nominal GDP which would offset the economic contraction that we anticipate for 2020 and beyond. This impact on GDP takes into account the work of numerous authors who have shown that the multiplier effect and velocity of circulation have a strong synchronicity in the transition process (see Dalziel 1996: Wang et al, 2010). Importantly, to further guard against the dangers of rampant inflation, the government should ensure that incremental amounts of the newly created money is progressively allocated between different components of GDP so that it boosts nominal GDP growth without any potential side effects on other macroeconomic variables. This will most likely happen if the government adopts a productive credit creation strategy as I have explained in the previous paragraph.

In normal circumstances, QE as a policy tool can become a powerful instrument in comparison to the current blunt interest rate tool used by the central bank. In fact, an understanding of the real mechanics of QE is likely to increase its acceptance, and I believe it is where macroeconomics must begin, i.e., “a new paradigm in macroeconomics”, from which Mauritius could be a beneficiary if properly understood and embraced by its policy makers.

Publicité

Publicité

Les plus récents