Publicité

The Mauritian Economy: In Critical Condition

Par

Partager cet article

The Mauritian Economy: In Critical Condition

This article reviews the current state of the economy with a focus on the major macro-economic indicators such as growth, the balance of payments, the fiscal deficit and public debt. It also highlights the risks of a potential financial crisis posed by unsustainable fiscal and external imbalances. Some positive signs of a recognition of the limits to fiscal profligacy are emerging, which may lead to eventual reforms and adjustments in economic policies.

Growth

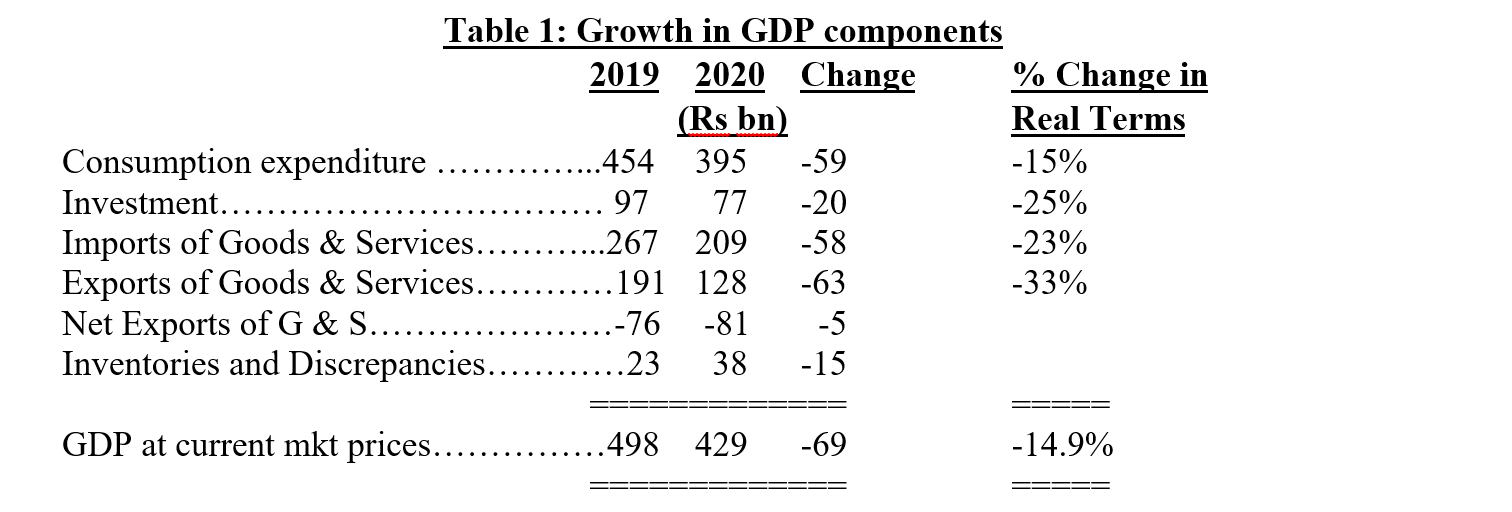

The advent of the Covid pandemic and the associated lockdown measures have impacted the economy severely in 2020, with negative real GDP growth close to 15%. The major sectors contributing to this downturn were services-related, such as Accommodation and Food Activities, Transportation and Storage, and Wholesale and Retail Trade. The decline in Construction and in Manufacturing was mostly concentrated in the second quarter of last year.

With a new lockdown announced in March 2021, the projected real GDP growth rate for 2021 is not likely to exceed 5%. Of the reduction of about Rs70 bn in nominal GDP in 2020, only about half will thus be recovered in in 2021. Assuming continuing average annual real growth of 5%, it would take until 2024 to return to the pre-Covid real GDP level of 2019.

The subdued level of inflation, at 2.5% in 2020, is mainly due to the marked contraction in the real consumption expenditure of Mauritian households by 18% in 2020, which has greatly eased demand pressure on prices. But the depreciation of the rupee and a recovery in consumption is expected to eventually fuel higher inflation of 5% in 2021.

Exports of goods and services fell sharply in 2020, but imports of goods and services dropped even more drastically as households cut back on consumption expenditure. Net exports of services decreased by Rs30 bn, mainly on account of tourism. Net imports of goods decreased by Rs25 bn, with exports lower by Rs9 bn, and imports by Rs34 bn. The net deficit on goods and services therefore deteriorated only slightly by Rs 5 bn.

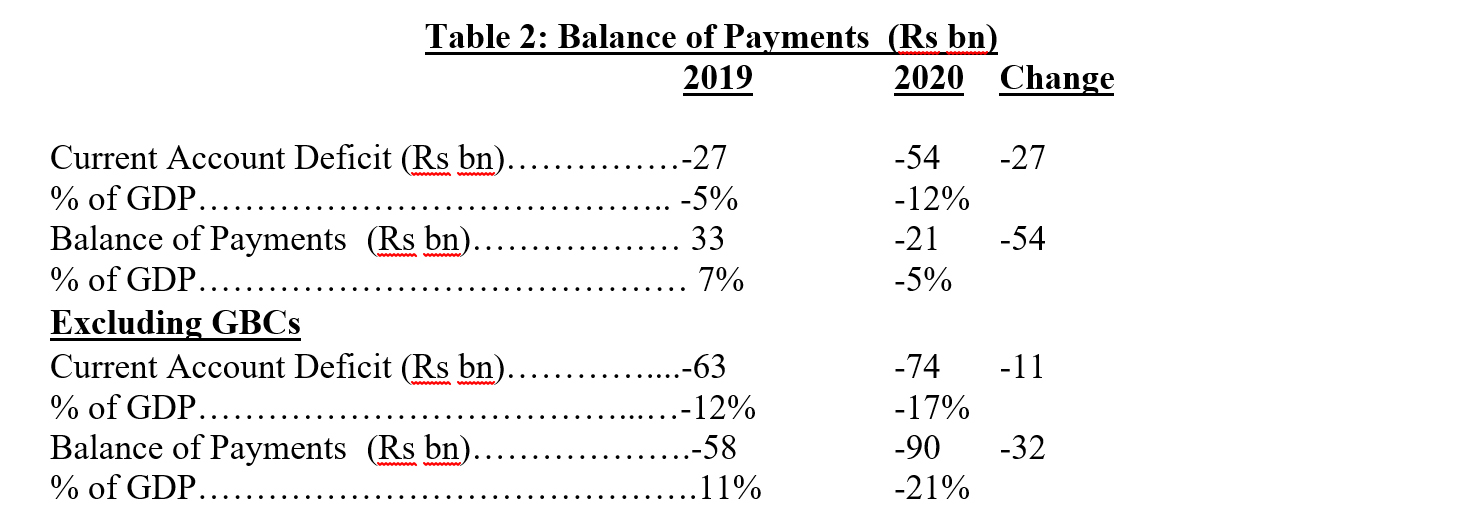

Other items on the external current account showed a smaller surplus by Rs 22 bn, chiefly due to lower direct investment income of Global Business Companies (GBCs). The external current account deficit doubled in 2020 to Rs54 bn, or around 12% of GDP, and is projected by the IMF World Economic Outlook (WEO) of April 2021 to rise further to Rs70 bn in 2021, or about 14% of GDP.

Balance of Payments

The overall balance of payments (BoP) worsened in 2020 by over Rs50 bn over the previous year to record a reserves deficit of Rs21 bn, the first deficit after more than a decade of surpluses. The BoP is heavily influenced by external flows of Global Business Companies (GBCs). In 2020, net inflows of GBCs on the current account fell by Rs17 bn. Total net inflows of GBCs declined by Rs22 bn, from Rs91 bn in 2019 to Rs69 bn in 2020. As a result, the balance of payments worsened in 2020 by more than would be the case without GBC flows.

Capital outflows, mainly on account of GBCs, represents a major risk of serious deterioration of the balance of payments and of external reserves. More than 60% of the total deposit base of banks consists of GBC and other foreign currency deposits, which have remained stable so far. But external vulnerabilities remain. So far, accommodative monetary policies in the U.S. and other advanced countries have sustained financial flows to emerging markets, but the threat of a rise in U.S long term interest rates and the likelihood of a reversal in U.S. monetary easing could be significantly disruptive for global capital flows, including to Mauritius.

Taking comfort from the high import cover of foreign exchange reserves can therefore be a misleading indicator of our reserve adequacy in view of the substantial size of potential capital outflows. The IMF has developed a measure of adequacy of reserve holdings, namely the ARA metric, which assesses the need for a country to hold precautionary reserves based not on its imports, but on other broader indicators of BoP risks, including external debt and equity liabilities, broad money, and export earnings. According to the IMF’s calculations, the foreign reserves of Mauritius currently meet only 36% of its minimum precautionary needs.

On the basis of an adjusted reserve adequacy metric, with less emphasis on GBC external liabilities, an IMF 2019 report on Mauritius concluded that its reserves were broadly adequate. The IMF added that, given the large size and complex structure of the GBC sector, Mauritius should continue to build reserves to establish stronger buffers against external shocks.

Gross official foreign exchange reserves were boosted during 2020 by sizeable external financing, and remained almost unchanged at slightly over USD7 bn between end Dec 2019 and end Dec 2020, and at March 2021. In rupee terms, reserves increased by about Rs19 bn between Dec 19 and Dec 20, mainly reflecting a depreciation of 11% in the effective rupee exchange rate.

The BoP reserves deficit was contained in 2020 by budget support loans of EUR188 mn from the African Development Bank (AfDB) in June 2020 (EUR188 mn), and from the Agence Francaise de Developpement (AFD) in July 2020 (EUR300 mn), totalling USD 550 mn, or Rs22 bn. Without this exceptional financing, the overall BoP would have recorded a deficit of over USD1 bn. Govt continues to raise new foreign loans and signed an agreement in Feb 21 with Japan under the AfDB’s EPSA programme to borrow Y30 bn, equivalent to about USD280, or Rs11.3 bn, for private sector development.

The 2019/20 budget provided for a flexible credit line (FCL) of Rs7.8 bn from the IMF, but Mauritius has not so far concluded a financing agreement. Mauritius would probably not qualify for FCL resources, which the access criteria include (i) sound public finances, including a sustainable debt position, (ii) effective financial sector supervision, and (iii) data integrity and transparency. Article IV consultations with the IMF have been initiated this month, and the prospect of entering into an arrangement with the IMF for financial support remains open.

Govt announced almost a year ago that over a quarter of foreign reserves held by the Bank of Mauritius (BoM), i.e., USD2 mn or Rs80 bn, would be utilized to fund the operations of Mauritius Investment Corporation (MIC). Although financing applications of Rs17 bn have been approved, only an amount of about Rs2 bn has been disbursed at early March 2021. A possible reason for the peculiarly slow disbursement is that the amended BoM Act also specifies that any amount invested in MIC shall no longer be included in official foreign reserves. Additional foreign financing to boost reserves may help to accelerate MIC disbursements.

Huge Fiscal Deficit

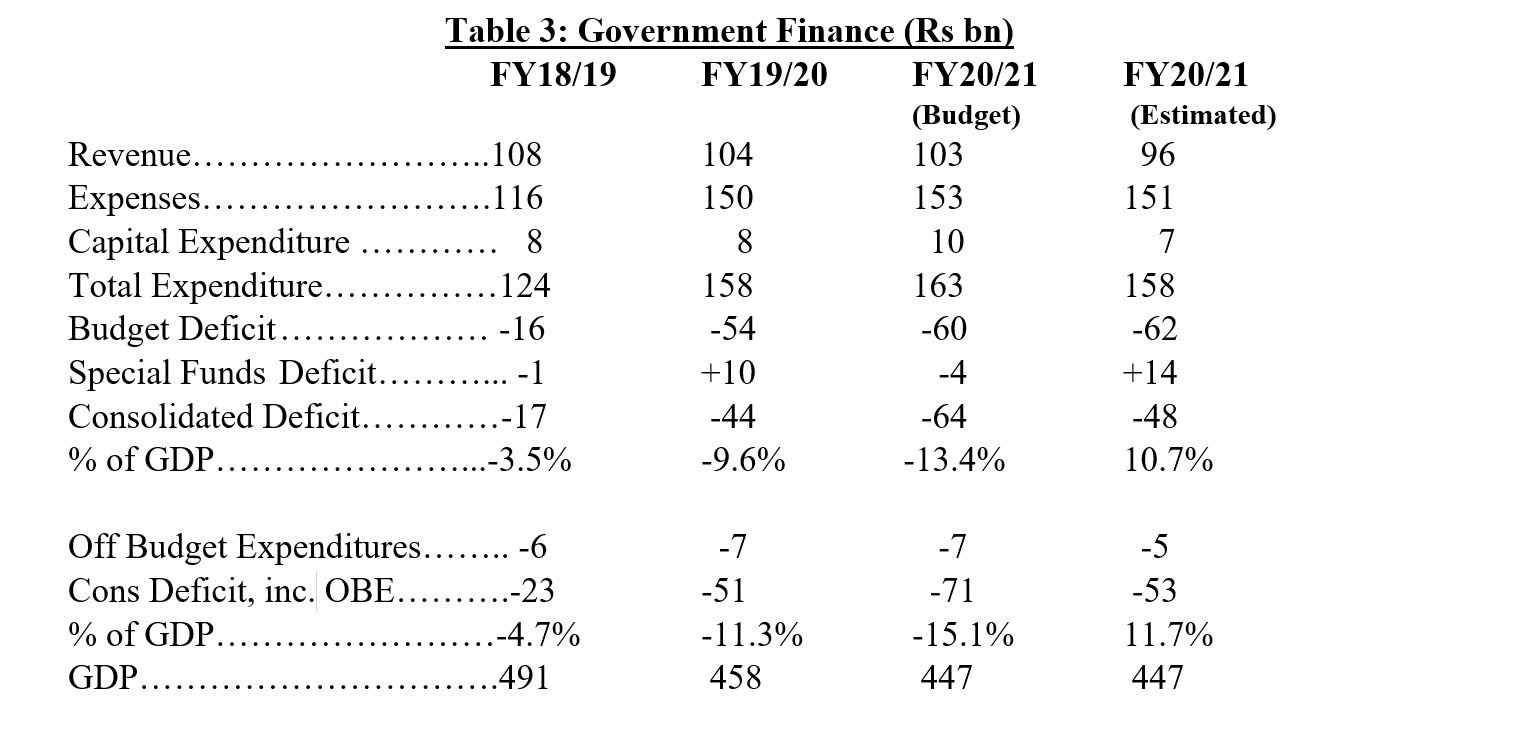

There is a growing lack of transparency in obtaining current fiscal data. The monthly statement of Govt Operations published by Statistics Mauritius provides a detailed breakdown of Govt expenses, normally with a 2-month lag. However, for this financial year 2020-21, data for only the month of July 2020 is available. Despite the increased recourse to special extra budgetary funds for Govt spending, there is no current information on expenditures by these special funds, including the Covid Projects Development Fund, to which a transfer of Rs15 bn was made from the 2020/21 budget, or the amount of Rs9 bn earmarked by the National Resilience Fund as financial support to the national air carrier.

Estimating the current fiscal outcome is therefore subject to a significant margin of error. The budget deficit for 2020/21, consolidated with special funds, is expected to be around Rs50 bn, or 11% of GDP, slightly higher than in 2019/20. Revenue in 2020/21 is projected at Rs96 bn, and total expenditure, including capital spending, would be contained to close to Rs160 bn, as in the previous financial year.

This forecast is based on (i) a shortfall in tax revenue of some Rs7 bn on the budgeted estimate, (ii) wage subsidies to employees and self-employed persons of Rs12.6 bn, or Rs4.5 bn over the budgeted level of subsidies (iii) savings of 5% on budgeted recurrent expenses, amounting to Rs6.5 bn, and (iv) little or no spending by special funds, resulting in a surplus of around Rs15 bn, corresponding to the amount transferred to the Covid Fund.

The IMF WEO of April 2021 foresees a broadly similar Govt deficit figure of Rs47.7 bn for 2020/21. Inclusive of off-budget expenditures (OBE) of about Rs5 bn, mainly of Metro Express, the budget deficit could be close to 12% of GDP. Govt is now injecting additional equity of Rs1.7 bn in Metro Express for an extension from Rose-Hill to Reduit through Ebene, for a total cost of Rs4.5 bn.

A 2020/21 Supplementary Appropriation Bill for Rs17 bn, initially introduced in the National Assembly at end 2020, and again in April 2021 provides for an amount of Rs11.9 bn as equity investment in the National Property Fund, and the remaining Rs6.1 bn mostly as recurrent expenditure. The additional equity investment will not add to the budget deficit, since it only represents the acquisition of a financial asset and is therefore not included in expenditure for computing the deficit.

This equity transaction is in effect a bail-out of former BAI companies, to meet the financial liabilities of National Property Fund, Maubank, and National Insurance Company, set up in the wake of the break-up of the BAI Group. Similar examples of Govt expenditures disguised as investments are the annual equity injections in Wastewater Management Authority, and in other state-owned companies that similarly fail to produce any financial returns over time. In effect, the expenditure of Rs11.9 bn should be added to Govt subsidies, widening the deficit gap in 2020/21 by another 2.5% of GDP.

Elevated Public Debt

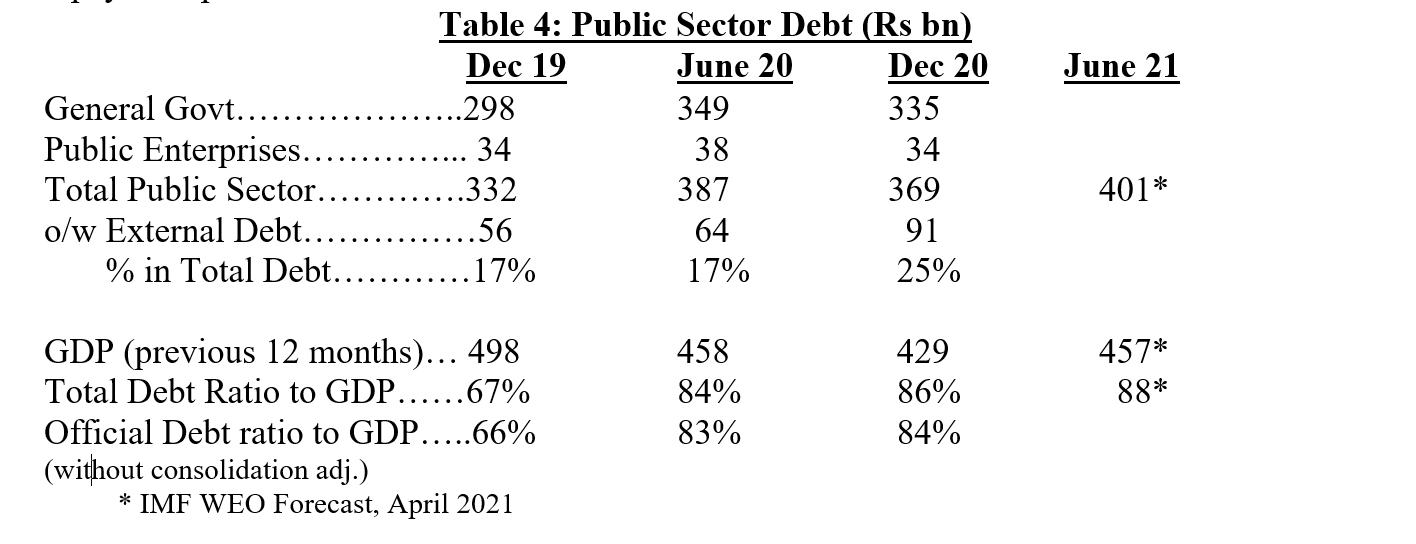

The financing of large fiscal deficits has led to an elevated level of public sector debt, amounting to Rs369 bn at Dec 2020, representing 86% of GDP. The IMF WEO, April 2021 projects that public sector debt will rise to Rs401 bn in June 2021, or close to 90% of GDP. The sustainability of public debt is increasingly questionable, especially since the growth outlook appears highly uncertain, notably as regards tourism.

Govt’s rising social expenditures have expanded financing needs, including a greater recourse to external resources. The share of external debt in total public sector debt increased from 17% in Dec 19 to 25% in Dec 20. Foreign borrowings by Govt from development institutions such as AfDB and AFD add to public debt, but on relatively advantageous terms, with long repayment periods.

Govt also relied heavily on the Bank of Mauritius (BoM) to limit the rise in public debt in the hope of avoiding a credit rating downgrade. In Dec 19, an amount of Rs18 bn was transferred from the BoM Special Reserve Fund (SRF) for prepayment of external debt, as provided by the amended BoM Act. However only Rs7.2 bn was prepaid in Jan 2020, and the balance used for Govt financing, pending other external debt prepayments in future years.

In April 2020, an amount of Rs15 bn was extended as credit to Govt by the BoM. In August and September 2020, BoM transferred a total amount of Rs60 bn to Govt as a one-off grant contribution to assist in stabilizing the economy. Although the amended BoM Act authorizes BoM to make such a grant to Govt from the SRF, this provision was not utilized. Instead, BoM announced the Govt grant would be raised from the domestic market by the issue of BoM securities for liquidity management. But the net amount of monetary policy instruments issued by BoM between end June 20 and end March 21 is about Rs 30 bn.

The BoM grant to Govt is deficit financing and not Govt revenue, in accordance with the IMF methodology on Government Finance Statistics. The ludicrous claim of a balanced budget based on BoM’s contribution of Rs60 bn can definitively be laid to rest. Encouragingly, the Minister of Finance recently announced that BoM will not resort to BOM grant finance again.

Moodys Credit Rating

In March 2020, Moodys downgraded Mauritius’ sovereign rating by one notch from Baa1 to Baa2, reflecting “the downside risks of a slow and prolonged Covid economic recovery” and “a sharp and long-lasting deterioration in fiscal and debt metrics”. Moodys considers that Mauritius’ fiscal response to the coronavirus shock has been one of the largest among its rated countries.

The rating outlook is negative. Moodys considers that a further downgrade is likely if there is a continued deterioration in (a) the relatively elevated debt burden, (b) the effectiveness of monetary policy due to increased BoM financing of the budget deficit and worsening inflationary risks, and (c) domestic and external imbalances, accompanied by price and rupee volatility.

The possibility of a further downgrading of the country’s rating by Moodys, which would throw Mauritian banks into junk grade status, could be deeply destabilizing for external capital flows. Further delay in getting Mauritius off the FATF greylist would also add to financial uncertainties. Renewed recourse to central bank money printing for fiscal purposes, accompanied by large and unsustainable fiscal deficits and mounting public debt, could seriously undermine investor confidence and aggravate external vulnerabilities.

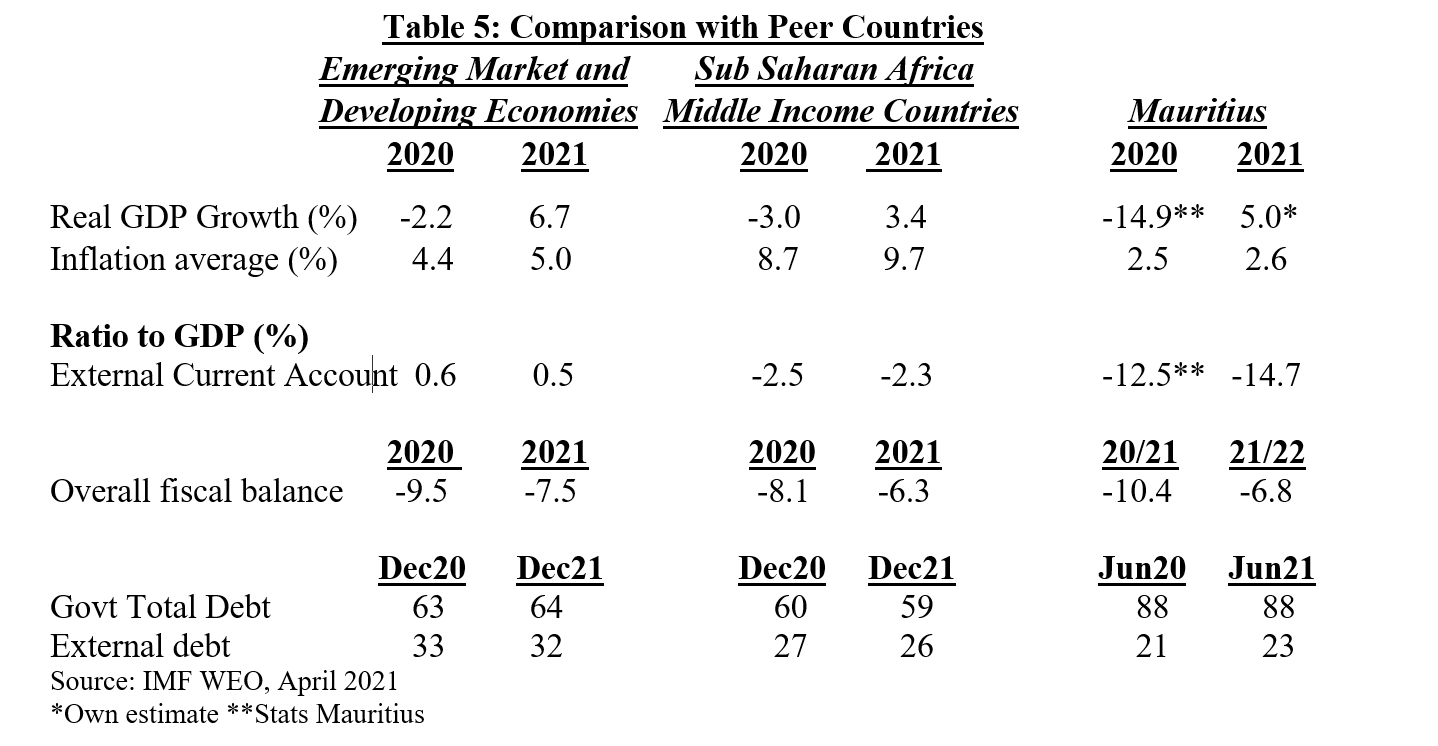

Credit rating agencies pay attention to relative economic performance in their country assessments. In a comparison with its peer countries, Mauritius fares worse on growth, the external current account, the overall fiscal deficit, and public debt. With a high negative GDP growth rate in 2020, Mauritius is among the worst-hit countries by the Covid pandemic, due to a high dependence on tourism. Reflecting a very open island economy with a heavy reliance on external trade, Mauritius also recorded a much wider external current account deficit relative to GDP.

The overall fiscal balance in relation to GDP is much higher in Mauritius than in peer countries in Sub-Saharan Africa, but is broadly comparable to the group of emerging market and developing economies. Adjusting for off-budget and other expenditures, Mauritius fiscal deficit would be even higher. Most noticeably, the public debt burden is considerably heavier in Mauritius than in peer countries.

The Moodys downgrade has forced a better realization of the escalating fiscal risks to financial stability. Govt appears to have made a recent policy U-turn by setting up a Committee on Sustainability of Public Finances to “come up with proposals to consolidate public finances in the immediate, medium and long term”, and “look into measures to reduce the budget deficit and public sector debt”. By embarking on a fiscal consolidation programme, Govt hopes to avert further downgrading by Moodys, and improve the country’s credibility with the IMF and other international lending institutions.

Conclusion

Hopefully, there is also a genuine awareness of the perilous financial risks associated with wasteful, reckless and populist economic policies. Already, there is a growing consensus that the country is overcome by acute governance issues, and is transmuting dangerously into an autocratic and kleptocratic state.

To meet the overriding concern about public debt sustainability in the aftermath of the Covid pandemic, a more responsible fiscal approach will become unavoidable. Without corrective fiscal adjustments, the pursuit of a vigorous economic recovery will be a futile endeavor.

Mauritius is at a critical juncture for determining its economic future. The economy is headed straight to the ICU unless decisive action is taken to nurse it back to health with deep and wide-ranging fiscal and economic reforms. For the effective implementation of this reform plan, an IMF financing arrangement supplemented by strong technical assistance may prove necessary, even if not desired.

Publicité

Publicité

Les plus récents