Publicité

Budget: Diving below the headlines (Part 2)

Par

Partager cet article

Budget: Diving below the headlines (Part 2)

In view of the forthcoming Budget which will be presented next Monday, the former Minister of Finance assesses the performance of Government after four and a half years.

Budget: Diving below the headlines (Part 1)

Budget: Diving below the headlines (Part 3)

Three great risks: lack of budget integrity,debt unsustainability and external vulnerabilities

Many reputed institutions and economic observers have sounded the alarm on the triple risks for the economy arising from

- the lack of integrity and transparency in the budget deficit;

- the unsustainability of the public sector debt and Government’s failure to meet its own statutory target for debt twice within few years ;

- the widening deficit on the external balances .

The accounting device to hide the true size of the budget deficit

The official budget deficit is estimated at 3.2 % of GDP in 2018/19 . However this figure does not include some recurrent and capital expenditures excluded from its computation , thus affecting fiscal integrity . First, there are special funds for the environment, national resilience and Lotto that represent Rs 4.31 b or around 0.86 % of GDP . Second, the subsidy on rice, flour and cooking gas is contained in the STC accounts and not in the budget . Third, there are sizeable capital expenditures incurred by state-owned enterprises and public entities that are kept outside the consolidated fund even if they are guaranteed by Government . Fourth, there are loans that are disguised as equity to escape inclusion in the deficit. In 2018/2019, such capital expenditures represent over Rs 15 b for the Metro Express and other projects financed by India and for the Mauritius Multisport Infrastructure Limited ( Côte D’Or sports complex) supported by China . It accounts for around 3 % of GDP. If all these recurrent and capital expenditures are recognised (which will have to be done one day), the budget deficit would be close to a staggering 7 % of GDP. In addition, there is an amount of Rs 12.5 b (2.5 % of GDP) to fund 6800 NHDC housing units announced last year. Also, the budget contains a substantial component of one- off grants in capital revenue which will not recur in future years. The estimates show such grants at Rs 9 b in 2018/2019, Rs 4.7 b in 2019/2020 and Rs 2.68 b in 2020/2021. Compared to 2018/19 , there will be a shortfall of around 1 % of GDP next year . Clearly the real budget deficit is much higher than the 3.2 % of GDP which is neither transparent nor credible.

The cynical subterfuge to lower public sector debt by stealth

The IMF and Moody’s, amongst others, have underscored the risks of the elevated and rising public sector debt which had reached 63.4 % of GDP in June 2018. The current Budget forecasts a slight reduction to 63.1 % at June 2019. The latest data released by the Ministry of Finance shows an increase to 64.8 % of GDP in March 2019 , 1.7 % higher than projected . The IMF forecasts that increased borrowing for spending will likely raise public sector debt to 67.5 % of GDP in 2019/20.

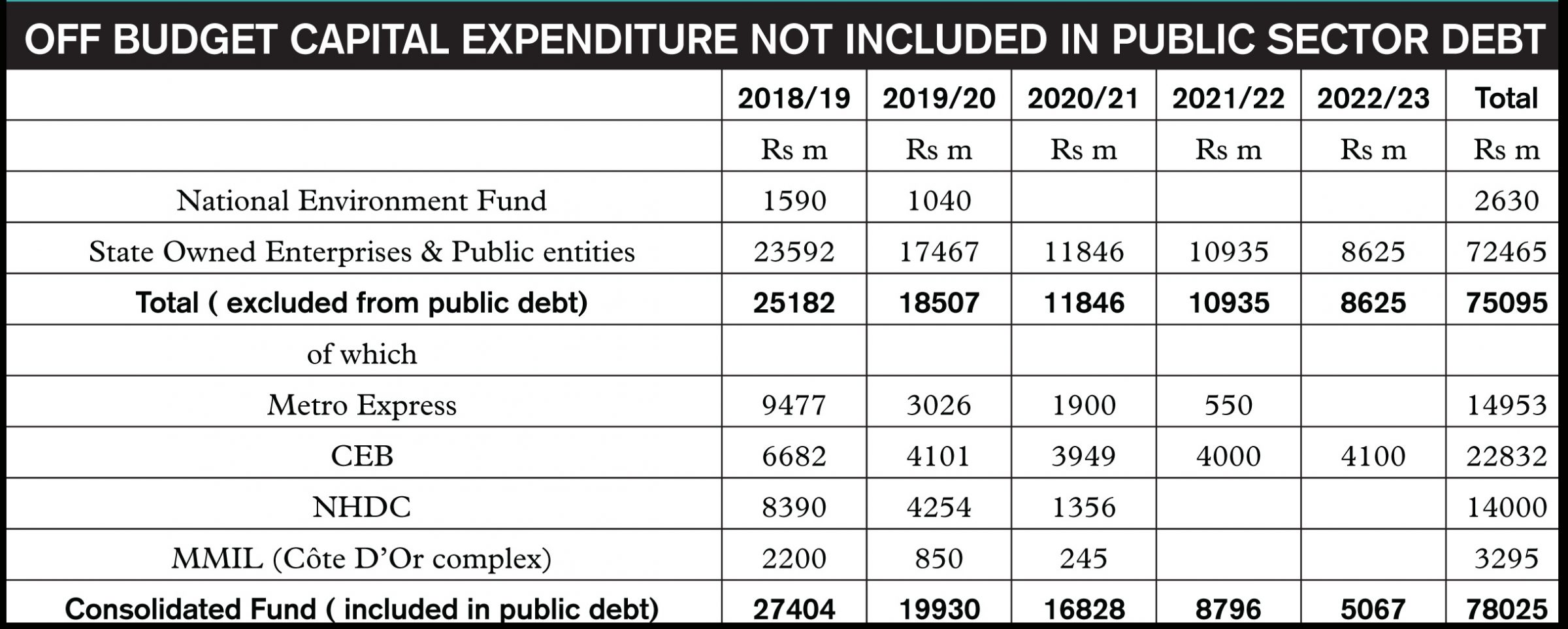

Even this high level largely underestimates the real size of the public sector debt as the liabilities of some SOE’s and public entities guaranteed by Government are not included in the calculation of the public sector debt. (See table)

The Metro Express investment of Rs 14.953 b financed by the Indian line of credit of US$ 500 m channelled through a SPV managed by SBM is not counted as public debt. The same applies for Rs 3.295 b to fund the Côte D’Or sports complex, Rs 2.63 for the National Environment fund and Rs 14 b to the NHDC. It should be noted that the above figures exclude the guarantee given to MT for the Safe City project costing around US$ 450 m and the sums advanced to Maubank, NIC and similar contingent liabilities. Many of these loans are characterised as redeemable preference shares or equity even if they are guaranteed by Central Government. If these actual debts, liabilities, guarantees and contingencies are reckoned, the public sector debt would escalate to above 70 % of GDP.

It is mind-boggling that capital expenditures financed outside the budget ( Rs 75 b or 15.5 % of GDP) and excluded from public sector debt over the five years are similar to the Rs 78 b investments included in the consolidated fund.

The necessity for a transparent and credible fiscal and debt management policy

Government has failed to meet its fiscal discipline objective. It agreed in 2015 to lower net public sector debt to a statutory target of 50 % of GDP at end 2018. It could not reach that objective as gross public sector debt was at 64.9 % of GDP in December 2018. This compelled it to postpone its attainment to June 2021. It has just realised that on current trend it would be impossible to meet the debt target of 60 % of GDP at June 2021 without significant policy adjustment . As expected , Government will choose the easy way out by further deferring the time line to reach the 60 % target by another two years to June 2023. Instead of taking the bull by the horns and introduce necessary adjustment measures to contain the debt surge.

The country urgently needs a sound, credible and sustainable fiscal and debt management strategy to support long term growth. Government has a responsibility to publish a comprehensive fiscal and debt risk analysis and management as part of the Budget process so that the country has a framework to gauge all the contingent liabilities and risks pertaining to the financing of off-budget expenditures , especially when they are underwritten by Government. Until they are formally incorporated in the Consolidated Fund, which will take some time.

An overwhelming surge in the trade deficit

As a result of the consumptiondriven growth strategy of government and the sizeable import content of its public investment programme, the balance of trade deficit has swollen to unprecedented level in 2018 at Rs 112 b , representing an astronomical 23 % of GDP . The ratio of exports of goods to GDP has fallen sharply from 24 % in 2010 to around 16.2 % today. Figures for the first quarter of 2019 show a trade deficit of Rs 27 b , a considerable rise of 28 % compared to the same period in 2018. It is forecast to widen further to Rs 129 b in 2019 or a colossal 25 % of GDP.

A high and widening current account deficit

The magnitude of the deficit of the trade balance is so exorbitant that even the surpluses in the services and the income accounts are not enough to contain and stabilise the deficit on the current account. As a result the current account deficit has risen sharply from 3.6 % of GDP in 2015 to 5.7 % in 2018. It is expected to deteriorate further to 8.5 % of GDP next year due to anaemic exports, rising imports and lower external grants. This is clearly unsustainable and there will be inevitable adjustments that could be both painful and disruptive of economic growth and stability .

Beware of the reversing trend in the balance of payments

As the current account deficit widens it will automatically worsen the balance of payments which has been posting a surplus for a long time. From 5.9 % of GDP in 2014 , the balance of payments surplus rose to 6 % in 2016 and 6.2 % in 2017 as a result of the substantial contribution of the global business sector and the good performance of tourism . However the surplus has declined swiftly in 2018 to 3.6 % of GDP at Rs 16.6 b . The trend is worrisome as the third and fourth quarters of 2018 posted an unexpected deficit in the balance of payments. The cumulative shortfall for the two quarters is at Rs 9.1 b . This pattern could continue in the January-March 2019 period with the rising deficit in the trade balance and the 10.6 % drop in tourism receipts . The consumption –led strategy and the huge import content of Government’s unsustainable investment programme is weighing heavily on the external balance even if Government may reap some additional receipts from consumption tax such as VAT and excise duties.

Gross international reserves are rising because of BOM intervention

Under normal circumstances the international reserves of the country depend on whether the external account posts a surplus or a deficit. As the balance of payments comes under pressure due to the sizeable trade deficit and lower tourism receipts , reserves will be adversely affected . It has already happened in the third and fourth quarters of 2018 with deficits of Rs 6.9 b and Rs 2.2 b respectively . The reserves resulting from the performance of the balance of payments came down by Rs 6.9 b and Rs 2.2 b as should be the case since it is the mirror image of the deficit . However the Bank of Mauritius intervened in the domestic foreign exchange market to buy US$ and sell rupees ( it bought around US$ 650 m in 2018) simply to accumulate international reserves and offset the decrease arising from the BOP deficit.

The Bank of Mauritius cautioned in its last BOP report that

- ‘the pick-up in reserve assets in 2018 emanated mostly from the net purchases of foreign exchange by the Bank from the domestic market, which more than offset the declines in foreign currency balances of both commercial banks and the Government held with the Bank’

So reserves are not growing because of rising export earnings for goods ,services and capital inflows but through the intervention of the BOM to purchase US$ in exchange of rupees to amass assets. Of concern and as shown by the same BOM document , all the proceeds from these interventions are not always sterilised as it is an expensive operation that varies between 2.50 % and 3.75 % per annum to the Central Bank. As a consequence it adds to the huge excess liquidity which distorts the transmission mechanism of monetary policy.

Budget: Diving below the headlines (Part 1)

Budget: Diving below the headlines (Part 3)

Publicité

Publicité

Les plus récents